What Are the Hidden Costs of Buying a House in Kansas City?

Buying a house is one of the most exciting milestones in life, but it’s also one of the biggest financial commitments. For homebuyers in Kansas City and surrounding suburbs like Prairie Village, Leawood, and Overland Park, the process goes far beyond just saving for a down payment and getting approved for a mortgage.

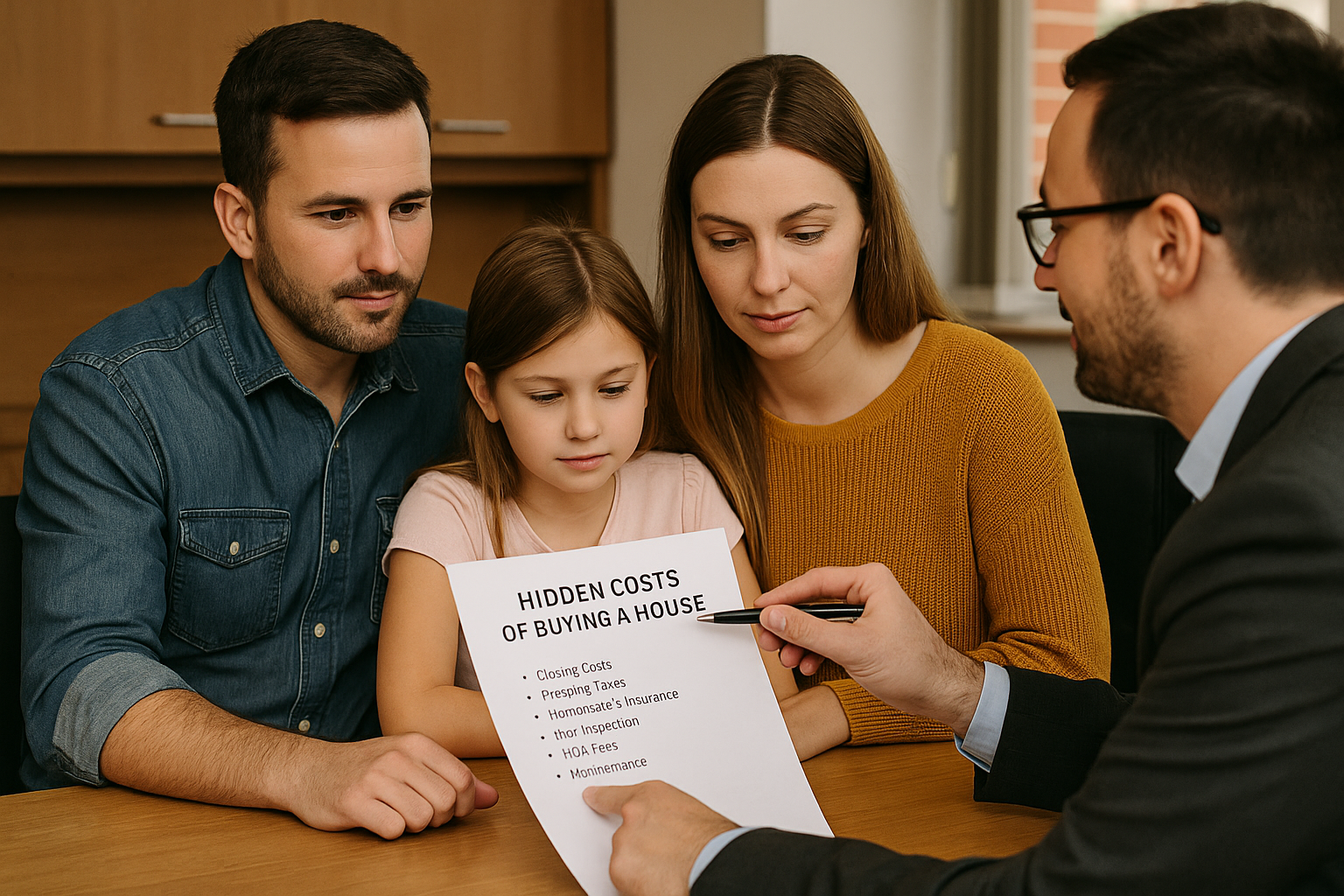

Many first-time buyers are surprised to discover the hidden costs of buying a house. From closing fees to ongoing maintenance, these expenses can add up quickly if you’re not prepared. Knowing what to expect—and working with the right lender—can help you budget confidently and avoid financial stress after move-in day.

The Mortgage Basics: Types of Loans to Consider

Before diving into hidden costs, it’s important to understand the types of mortgages available in Kansas City:

Conventional Loans

-

Best for buyers with strong credit scores.

-

Down payments can range from 3% to 20%.

-

Less than 20% down requires private mortgage insurance (PMI).

FHA Loans

-

Designed for first-time buyers or those with lower credit scores.

-

Require as little as 3.5% down.

-

Easier qualification, but include ongoing mortgage insurance premiums.

VA Loans

-

Available to veterans, active-duty service members, and eligible spouses.

-

No down payment, no PMI, and competitive rates.

-

A great option for military families in the Kansas City metro.

USDA Loans

-

Geared toward homes in rural or suburban areas.

-

No down payment required, but income restrictions apply.

-

Could be an option for homes on the outskirts of Overland Park or near smaller Kansas towns.

Fixed vs. Adjustable Rates

-

Fixed-rate loans: Same payment over 15–30 years; best for long-term homeowners.

-

Adjustable-rate mortgages (ARMs): Lower starting rates but can increase after an introductory period; best if you plan to move within a few years.

Understanding your mortgage options is key, but don’t stop there—the real costs of homeownership are often in the details.

The Hidden Costs of Buying a House

1. Closing Costs

One of the biggest surprises for first-time buyers is closing costs. These typically range from 2%–5% of the home’s purchase price.

In Prairie Village or Leawood, where homes often cost more than the metro average, closing costs can add thousands to your upfront expenses. Common fees include:

-

-

Loan origination fees

-

Title insurance

-

Appraisal fees

-

Attorney fees

-

Escrow deposits

-

Tip: Ask your lender for a detailed estimate early so you’re not caught off guard.

2. Private Mortgage Insurance (PMI)

If you put down less than 20%, you’ll likely be required to pay PMI until you reach enough equity. This can cost between $50 and $200 per month, depending on your loan size.

3. Property Taxes

Kansas City spans multiple counties (Johnson, Jackson, Wyandotte, etc.), and each has different property tax rates. For example:

-

-

Homes in Overland Park (Johnson County) often carry higher taxes due to property values.

-

Homes in Prairie Village and Leawood also lean higher-end, which means higher annual bills.

-

Be sure to factor this into your monthly mortgage estimate.

4. Homeowners Insurance

Insurance premiums vary depending on the size, location, and age of the home. Older homes in Kansas City may require more coverage due to roof condition or foundation concerns. Expect to pay around $1,500–$2,500 per year in this region.

5. Home Inspections and Repairs

Before closing, you’ll need a home inspection to identify potential issues. This typically costs $300–$500. However, the bigger expense comes if problems are uncovered:

-

-

Roof repairs

-

HVAC replacements

-

Foundation cracks

-

Buyers in Leawood or Prairie Village, where many homes are older, should be especially mindful of potential repair costs.

6. HOA Fees

If you buy in a neighborhood with a homeowners association, be prepared for monthly or annual HOA fees. In Overland Park and surrounding areas, fees can range from $25 to several hundred dollars, depending on amenities.

7. Utilities and Upgrades

Utility costs in Kansas City vary by season. Summers can mean high electricity bills for air conditioning, while winters may bring higher gas bills.

Additionally, most homeowners want to make updates:

-

-

Painting

-

Landscaping

-

New flooring

-

Appliance upgrades

-

These aren’t required, but they’re common—and they add to your initial expenses.

8. Ongoing Maintenance

Experts recommend budgeting 1% of your home’s value annually for maintenance. That means if you buy a $300,000 home in Overland Park, you should plan on at least $3,000 per year for repairs and upkeep.

Why Choose a Small, Local Bank for Your Mortgage?

When looking at all these costs, one of the smartest moves you can make is choosing the right lender. While national lenders may seem appealing, working with a small, local bank in Kansas City has distinct advantages:

-

Personalized customer service: Instead of a call center, you’ll meet with local loan officers in person.

-

Local expertise: They understand neighborhoods like Prairie Village, Leawood, and Overland Park and can provide insights on property values.

-

Community focus: Local banks reinvest in the area, supporting small businesses and community projects.

-

In-house servicing: Many local lenders continue to service your loan after closing, so you won’t be handed off to an out-of-state company.

-

Faster closings: Local lenders can often move quicker, which is a huge advantage in competitive Kansas City markets.

Common Questions People Ask

-

- How much should I save before buying a house in Kansas City?

Beyond the down payment, save at least 2%–5% of the purchase price for closing costs, plus extra for moving and immediate updates. - What’s the average down payment in Overland Park or Leawood?

While 20% is ideal, many buyers put down 5%–10% and use PMI until they reach enough equity. - Are property taxes high in Kansas City suburbs?

Johnson County suburbs like Leawood, Prairie Village, and Overland Park tend to have higher property taxes than other parts of the metro, due to property values and schools. - Should I get pre-approved before house hunting?

Yes. Pre-approval shows sellers you’re serious and helps you understand your true budget. - What is the biggest hidden cost when buying a home?

For most buyers, it’s a combination of closing costs and ongoing maintenance. Many new homeowners underestimate how much it costs to maintain a property each year.

- How much should I save before buying a house in Kansas City?

Buying a home in Kansas City, Prairie Village, Leawood, or Overland Park is an exciting step, but it’s important to plan for more than just your mortgage payment. Closing costs, property taxes, insurance, HOA fees, and maintenance can add up quickly if you don’t budget for them in advance.

The good news? With the right preparation—and the right lender—you can navigate these expenses smoothly. Working with a small, local bank in Prairie Village ensures you’ll get personalized service, expert local knowledge, and in-person support from a team that cares about your community.

When it comes to buying a home, knowing the hidden costs is half the battle. Plan ahead, ask the right questions, and choose a trusted Kansas City lender to guide you through the process. That way, when you finally get the keys, you can enjoy your new home with confidence and peace of mind.

Trusted Local Bank for Car Loans, Business Loans, Personal Loans, Mortgages and More!

At First National Bank, we’re proud to serve the communities of Miami, Johnson, and Cass County with personalized, hometown banking. Whether you need personal and business loans, checking and savings accounts, CDs, IRAs, safe deposit boxes, or cash management services, we have you covered. Looking for home financing options? We offer mortgages, home equity loans, construction loans, refinancing, second mortgages, and swing loans to fit your needs. Stop by one of our convenient locations in Louisburg, Stilwell, or Prairie Village—or reach out to us today to learn how we can help you reach your financial goals.